Early Exercise & Founder-Trap Equity Decisions

Option Windows, Acceleration, and Advisor Equity

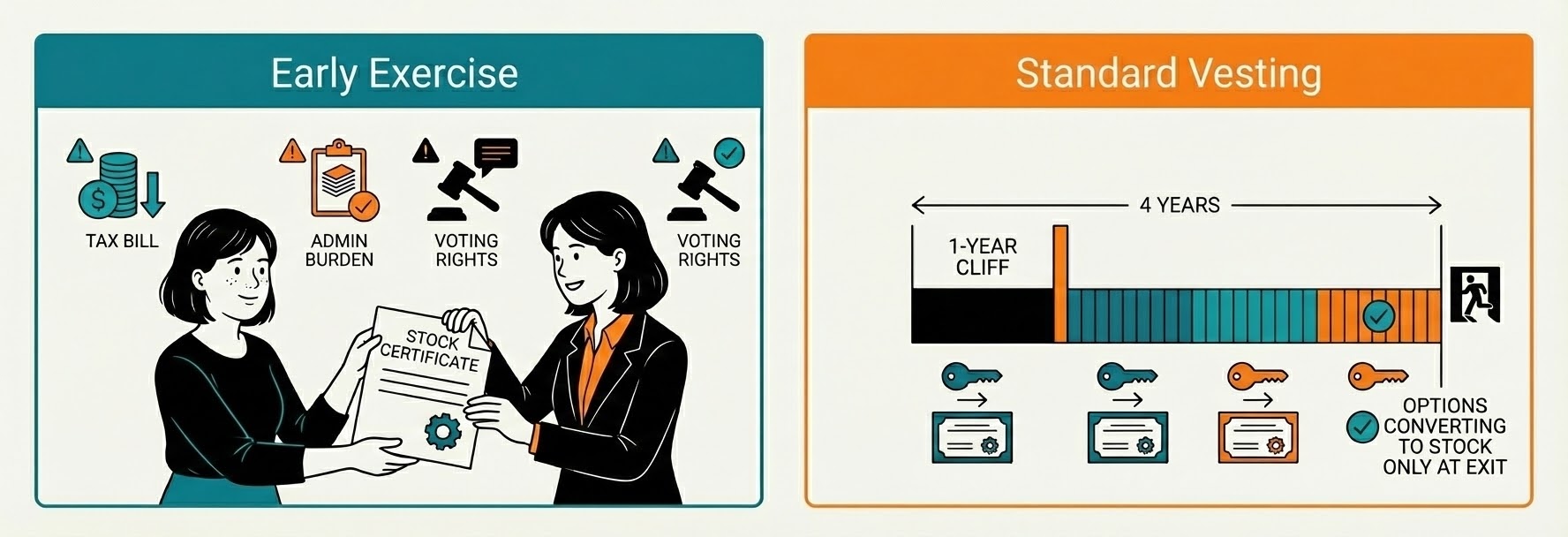

For US-based B2B founders (Angel → Series A): early-exercise equity decisions that seem employee-friendly in theory and might become company-hostile in practice.

TL;DR

Early exercise is almost never worth it for the company.

Long post-termination exercise windows mostly help people who already left.

Acceleration clauses create future cleanup and deal costs.

Early exercise MIGHT save employees on taxes, but it WILL cost your company something.

Early Exercise (Why We Rarely Recommend It)

We generally do not recommend offering early exercise, except in narrow circumstances.

Why Early Exercise Doesn't Help Much

From the employee's perspective:

Early exercise turns them into a stockholder sooner

That creates immediate tax liability

They still have to pay cash to exercise

Result: They often end up in the same economic position—after writing an extra check.

Why Early Exercise May Create Company Friction

From the company's perspective:

Exercised employees become stockholders

That creates administrative burden (meetings, consents, notices)

They gain voting rights

They get access to stockholder records

These stockholders usually own too little to matter for votes—but enough to matter if they become difficult

Warning: In some cases, early exercise increases the magnitude of headache a problematic employee can cause.

When Early Exercise Might Make Sense

While every company is different and talking to a specialized lawyer can get you the best answer, we GENERALLY only consider early exercise if all of the following are true:

The employee has a long, positive performance record

They have never raised a dispute

You are confident they will vote with the company's best interests

If any of those are shaky, early exercise is usually a net negative.

Option Exercise Periods (The 90-Day Debate)

Many founders ask whether the standard 90-day post-termination exercise window is "unfriendly" to employees.

Some companies propose:

If the employee worked ≥ 2 years → can exercise anytime before option expiration (typically 10 years)

If < 2 years → standard 90 days

Your plan permits the board to set exercise windows at grant, so this is legally feasible.

Why the "Employee-Friendly" Framing Is Misleading

This debate is often misplaced.

Recruiting Impact

Most employees don't know this clause exists

Fewer still evaluate offers based on it

Who Actually Benefits

The exercise window only matters if someone:

Quit, or

Was terminated

For a friendly, high-performing person who still believes in the company:

The only thing that changes with more time is their financial position

That usually improves only if they took a higher-paying job elsewhere, or went full-time on another venture

Why Longer Windows Hurt the Company

Longer exercise periods:

Keep disgruntled former employees on your cap table

Create ambiguity during financing

Create ambiguity during exits

Increase legal fees when acquirers ask: "Who can still exercise?" and "Who needs to be paid off?"

This ambiguity routinely turns into real dollars paid to lawyers.

Bottom line: Giving someone a small, abstract benefit they don't know they're getting—at the cost of future friction—is usually not worth it.

"Cashless" or Assisted Exercise (What People Mean)

People sometimes ask about "cashless" or upfront exercise.

What this usually means:

The board provides a bonus to offset or replace the exercise cost

It is not truly cashless—it's a compensation decision.

Managing Exercise Costs for Large Grants

Options you can socialize with senior hires:

Stay with the company long-term

Do not exercise until an exit or liquidity event

Avoid paying cash until there is clear upside to offset the purchase price

83(b) Elections (Common Confusion)

Critical Clarification

83(b) elections do NOT apply to options

They apply only to restricted stock, including restricted stock issued upon early exercise of an option.

For Non-US Residents

There are additional hiring and option-grant issues

ISO treatment may not apply

These should be discussed separately

Acceleration Clauses (Single / Double Trigger)

For Executives

Generally not advised

Even when used, investors often require founders to remove them pre-investment

For Advisors / Consultants

Strongly not advised.

Key risk: Non-founders ending up with more favorable vesting than founders or senior contributors—then later paying legal fees to undo acceleration provisions.

Advisors vs. Consultants (Paper vs. Reality)

If the relationship is advisory in substance, but:

No day-to-day involvement

Specific guidance on request

Then using consulting agreements can be cleaner:

Better IP assignment

Easier administration

Assuming US-based individuals. If outside the US, this changes.

Advisor Vesting (There Is No "Standard")

The idea that advisors "typically" vest over 2 years with no cliff is false. The closest thing to a reference is the YC FAST template—which offers a matrix, not a rule.

Common Patterns

Advisors making major, immediate contributions often vest monthly with no cliff

Advisors who stick with the company long-term are treated the same whether they have longer vesting or a cliff—the only difference is for someone who leaves quickly

We find more founders regret equity grants than wish they had given more, or faster vesting

Structuring the Relationship

It's helpful to specify:

A specific role (not just "advisor")

Expected number of hours or deliverables

How long you actually need them

Options vs. Restricted Stock for Advisors

Advisors may prefer the tax treatment of restricted stock. However, the same considerations that apply to employee incentive compensation also apply to advisors:

Early stockholders create administrative complexity

Voting rights and access to records come with stock ownership

Tax timing can matter, but so does company flexibility

Important: The advisor agreement itself does not grant stock or options. There's a separate legal process that does that—board approval, signed grant documents, and (for stock) payment of the purchase price.

FAQ

Q: Is early exercise good for employees?

A: Often no. It has the potential to create tax liability without changing exit economics.

Q: Should we extend exercise windows?

A: It mostly benefits people who already left and creates cap table ambiguity.

Q: Can employees file 83(b) on options?

A: Usually, no. Only restricted stock, including stock issued upon early exercise of options, qualifies.

Q: Is there a standard advisor vesting schedule?

A: No.

Bottom Line

Most "nice" equity tweaks feel generous today and expensive tomorrow.

Equity decisions compound.

If This Page Made You Nervous (That's Normal)

7 days free on any plan. No charge until you’re ready.

Get Automated Legal with Aegis

Subscribe to Aegis to build your cap table automatically — see your ownership breakdown, equity classes, and investment history organized from your documents.

We're lawyers, remember? Please read this important note:

Story LLP is a law firm, and Story's lawyers built Aegis to deliver better, standard legal services at scale so founders can choose between top-tier specialized lawyers and standardized process automations that replicate those lawyers according to their needs and budget. By definition, a standardized process may not be perfect for you. Please review our Policies page to better understand the difference, as well as how we use AI and how we manage conflicts, privilege, etc.

As a law firm, we must screen clients for conflicts of interest, and we treat all correspondence with clients seeking legal advice as privileged and confidential to the maximum extent possible in consideration of any conflicts. However, Story's law firm or our Attorney Allies do not represent you or your company as your lawyer, do not have an attorney-client relationship with you or your company, and do not provide you with legal advice absent a formal Engagement Letter signed between you and the Story LLP law firm. Please don't confuse the free knowledge we offer on this site with legal advice for you.